Chapter 4: FY 2020-21 Fund Balance

4.0 Fund Balance: Chapter Overview

- Components and calculation of fund balance

- Restricted vs. Unrestricted Funds

- Purpose of maintaining fund balance

4.2 Growth and Use of Institutional Fund Balances

4.3 Year End Fund Balance by Fund Type

4.4 Year End Fund Balance by Division

- Academic Affairs

- Advancement

- Business & Financial Affairs

- Enrollment & Student Services

- President

- University Relations & Marketing

- Institutional Budget

4.1 What is Fund Balance?

Fund balance represents the available resources of the fund as of a certain point. In this chapter, we report fund balance at the end of each fiscal year. It is important to note that the ending fund balance does not necessarily represent spendable cash. Rather, this represents the total value in the fund which may be comprised of available cash, capital assets, or other interest amounts within the fund that may be subject to certain restrictions.

The year end fund balance considers all activity within the fund and is calculated by the following formula:

Beginning Fund Balance + Revenues + Fund Additions - Expenditures - Fund Deductions - Transfers = Ending Fund Balance

Beginning Fund Balance: This is the balance of the fund as of the end of the previous fiscal year, and is a separate entry made by accounting services at the beginning of each fiscal year. This amount encompasses all prior activity of the previous year including revenues and fund additions, and expenditures and fund deductions. This amount represents the available resources of the fund at the beginning of the fiscal year, though not all may be spendable cash.

Revenues: This includes all external university revenues as well as all interdepartmental support activity in the fund during a given fiscal year.

Fund Additions: Although this is not true revenue, the effect of fund additions on fund balance is the same as revenue because this activity increases fund balance. These entries pertain to capital activity and are included for financial reporting purposes to keep the balance sheet in line. These amounts primarily consist of capital assets that are acquired by Western but not yet used for operations. For example, in FY21 the asset amount for the Interdisciplinary Sciences building is included as a fund addition entry. Once the building is open and in use for instruction, Accounting Services will show the building as a depreciable asset.

Expenditures: This includes all activity for expenses occurred in the fund during a given fiscal year.

Fund Deductions: Similar to fund additions, fund deductions pertain to capital asset activity. Fund deductions have the same effect on fund balance as expenditures, and represent remaining debt on capitals projects not yet in use. Entries for fund deductions are required for the balance sheet for financial reporting purposes.

Transfers: This activity represents transfers of expenses or transfers of fund balance to cover expenses during a fiscal year. Transfer activity sums to zero across all funds but has the net effect of increasing or decreasing fund balance when viewed across different funds, divisions, or departments. A transfer with a negative amount has the effect of increasing fund balance and reflects a reduction to expenses, whereas a transfer with a positive amount has the effect of reducing fund balance (because it increases expenses).

Ending Fund Balance: Conceptually, this amount represents the available resources of the fund at the end of a fiscal year, and includes all activity during the fiscal year, but does not equate to cash on hand. Much of the fund balance consists of capital assets.

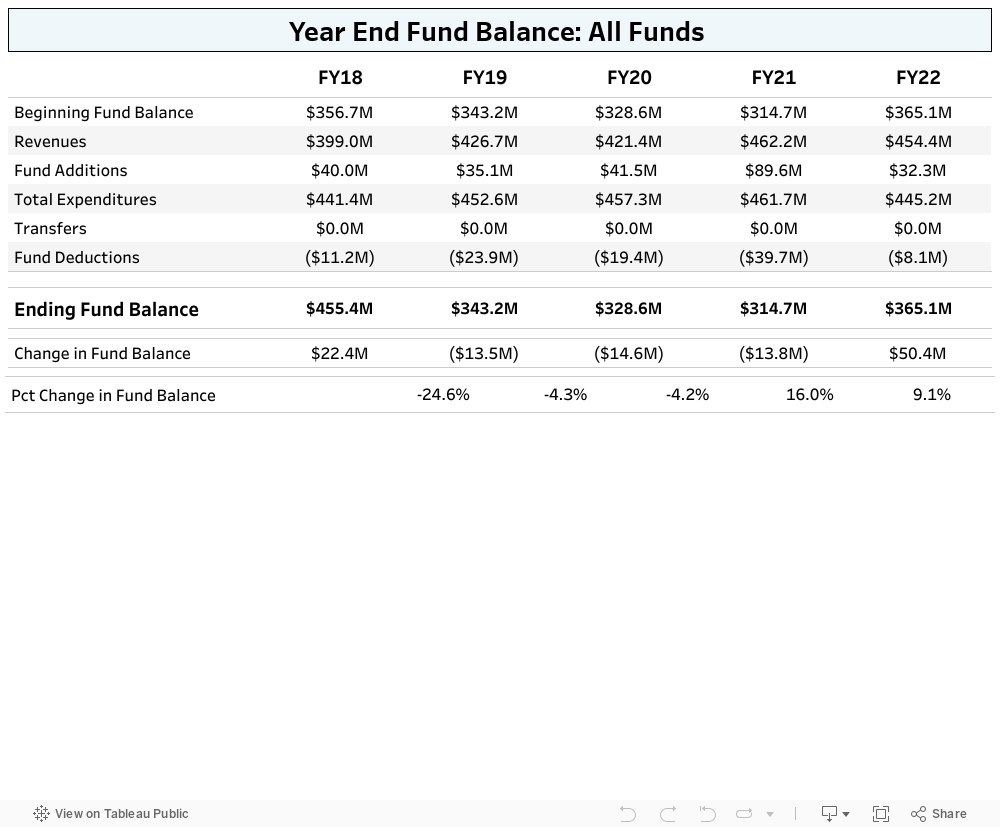

Fiscal year activity that results in the year end fund balance is shown in Table 4.1. The ending fund balance reflected in the table and internal financial reports is equivalent to the Net Position values reported in Western's annual Financial Statements. As discussed in Chapter 3, transfers reflect internal redistributions and have a net-zero impact on institutional fund balance.

Table 4.1 Year End Fund Balance Determination

Historical year end revenues, expenditures, and fund balance for all Chart 1 funds, matching the figures presented in the WWU Financial Statements.

4.1.a Fund Balance Exists at the Fund Level

The fund balance exists at the fund level and in some cases, funds may be shared across orgs (departments). Although many funds are specific to a given department or area, some areas share the same fund. Western’s chart of accounts does not require a default org for a given fund nor does it require a one-to-one fund to org combination. This is important to bear in mind because this structure makes calculation of fund balance at the department level difficult to impossible. Funds are linked to a default division, but this association is manually maintained and updated.

Because the fund balance exists at the fund level and not at the fund-org level, it is difficult to parse out ending fund balance by department for cases in which a fund is shared across departments. We have assigned all activity in a fund to a division using the default org code listed in Banner but please be aware that analysis at the fund level in this chapter may not match prior activity shown (expenditure, revenues) by division because there are instances in which funds have shared activity across divisions.

4.1.b Restricted vs. Unrestricted Fund Balance

The ending fund balance of a given fund does not necessarily represent available cash. Many funds have restrictions, are purposed for specific uses, or represent the net worth of an asset. For example, capital assets such as buildings have the value of the asset recorded as revenue in Western’s chart of accounts to reflect the value of the asset over it’s usable life according to a depreciation schedule. This is done for financial reporting purposes for the financial statements. Similarly, some funds maintain a balance but are not discretionary cash for the university, such as balances on endowment funds.

Some funds are not legally restricted (as in the case of endowment funds) but may be committed for specific purposes such as institutional funds that are committed for WWU capital projects.

4.1.c Purpose of Maintaining Fund Balance

Western maintains fund balances to buffer against unforeseen expenses that may occur such as contingencies (e.g., unanticipated emergencies such as equipment needs during the COVID-19 pandemic) or from uncertainties in state funding (e.g., to keep the university operations continuing in the event of delays for the legislature to pass a budget bill).

In addition to the University’s institutional fund balance, each division is allowed to maintain a divisional fund balance that serves the same purpose for divisional needs. Divisional fund balances accumulate through the recapture, or “sweeping”, of unspent departmental state funds in a given year. Some funds, such as grants & contracts awards or specific legislative appropriations cannot be moved to central divisional reserves and must be left in the departmental funds for which they are purposed.

4.2 Growth and Use of Institutional Fund Balances

4.2.a Factors in Growing Institutional Fund Balance

Between 2013 and 2016, several factors led to growth in the University’s Institutional Reserves balance:

-

Academic year tuition revenues exceeded budgeted figures due to higher than budgeted enrollment growth, particularly in non-resident undergraduate students.

-

The University’s general practice was to budget 98% of forecasted tuition revenues to ensure fiscal responsibility. Any unspent tuition surplus contributed to institutional cash reserves to help establish a balance that could support continued operations for one academic quarter in case of a major catastrophe.

-

The University maintained a recurring operating contingency budget at a level that was seldom fully utilized, resulting in contributions to institutional reserve balance at each years’ end. Beginning in 2016, the recurring operating contingency was reduced to $1,268,675 with the remaining amount built into the University operating budget as a source of funds.

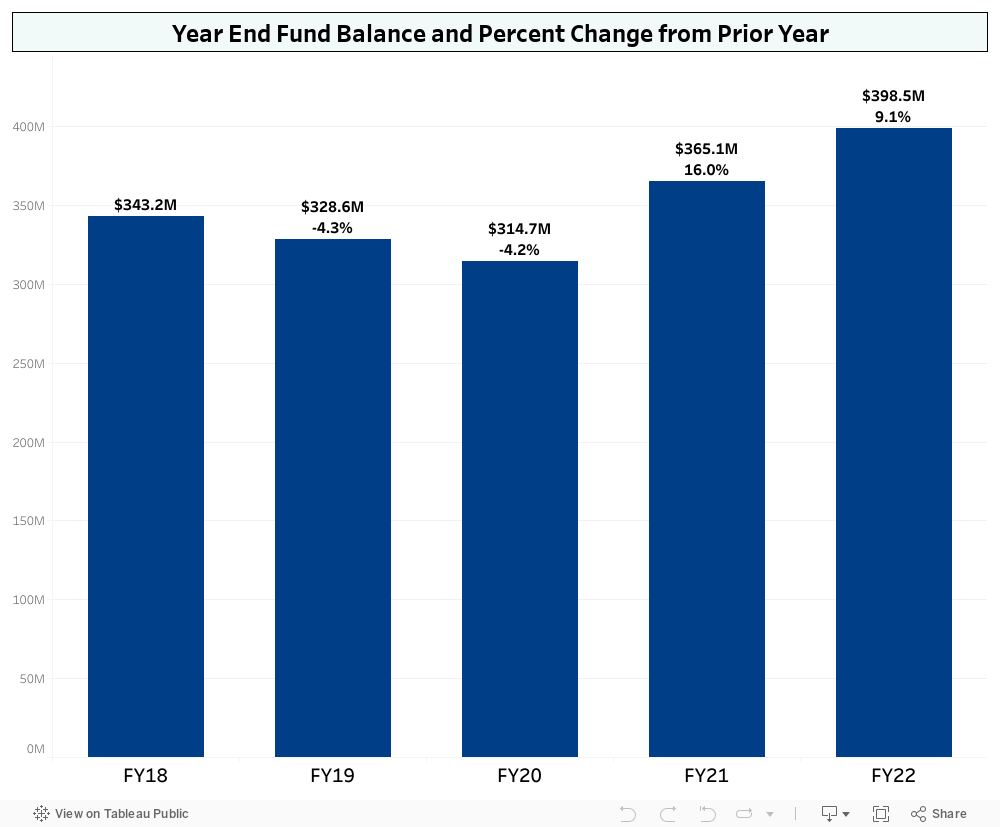

Figure 4.2 Institutional Fund Balance History

Year end fund balance for all funds and the percent change of ending fund balance from the prior year. The FY 2021 institutional fund balance includes capital revenue associated with building projects and the pandemic stimulus funding.

4.2.b Decisions for Use of Fund Balances

Institutional reserves were used between 2018-2020 to help fund a number of one-time priorities, including:

-

Completing construction of Carver Academic Facility

-

Disability Access Center

-

Multicultural Center

-

Implementation of Banner 9 Upgrade

Additionally, the University assumed an operating budget deficit in FY 2020 and has used reserves to bridge the gap until enrollment growth brought revenues to fund investments. WWU’s reserve balance allowed the University to mitigate uncertainty and financial impacts from the COVID-19 pandemic. This allowed the WWU to meet the initial fiscal impacts of the pandemic of the without implementing layoffs or furloughs in response.

Table 4.2 Institutional Budget

Fund balance includes state operating, dedicated local, auxiliary, and grants and contracts fund types.

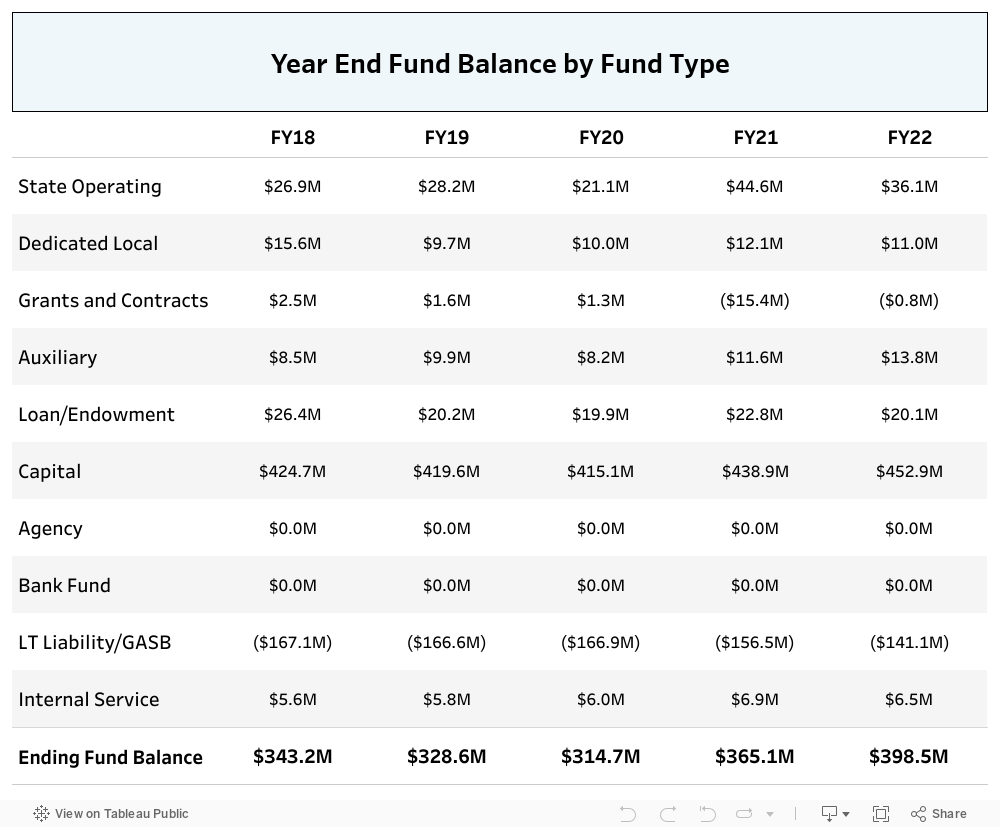

4.3 Year End Fund Balance by Fund Type

Western's annual Financial Statements report net position by fund type, which is equivalent to the fiscal year end fund balance. The Financial Statements include all fund types; however, in this chapter we focus on State Operating Funds, Dedicated Local Funds, Grants & Contracts, Auxiliary, and Capital funds because these funds represent resources related to Western's core mission and operations.

Fund Type Descriptions

Includes the remaining balance of unspent funds for state appropriations and tuition revenue. The balance is essentially cash, and unrestricted. For FY 2021, this balance shows higher than prior years because of the timing of drawing down HEERF funds.

In WWU's chart of accounts, these are fund types 11 and 14 in Chart 1.

This represents the accumulated unspent balance of funds in self-sustaining fee revenue funds and is essentially a cash balance and unrestricted.

In WWU's chart of accounts, this is Fund Type 12 in Chart 1.

These funds are established to charge departments their portion of shared expenses such as utilities and computing expenses. The ending balance is cash and unrestricted.

In WWU's chart of accounts, this is Fund Type 13 in Chart 1.

Fund balance in Grants & Contracts funds are restricted. Unspent funds can only be used under the allowances of the grant. For FY 2021, the negative balance in these funds are due to the timing of drawing down of HEERF stimulus funds.

In WWU's chart of accounts, this category encompasses fund types 21, 22, and 23 in Chart 1.

This includes the unspent balance of funds for Western’s auxiliaries, such as housing & dining. For FY 2021, the fund balance shown for Auxiliaries includes the transfer of HEERF Stimulus funds. The balance is unrestricted.

Auxiliary funds are all funds under fund type 31 for Chart 1 in WWU's chart of accounts.

Fund balances in Loan, Endowment, and Quasi-endowment funds are restricted. These balances encompass the principle of the loan or endowment, plus any interest earned on these investments.

This category includes fund types 41, 51, and 61 for Chart 1 in WWU's Chart of Accounts.

The balance on capital funds represents the value of Western’s capital assets. It does not represent spendable cash and all funds are restricted. The balance is the value of the assets less any debts. Assets that have already been expended against a depreciation schedule (such as building like Old Main) are not included, though non-depreciable assets such as land are included.

For purposes of this report, this category includes fund types 91, 92, 93, 94, 95, 96, 97, 98, and 99 in Chart 1 within WWU's Chart of Accounts, but we recognize that not all of these fund types represent activity directly related to Capital Projects.

Agency funds are pass-through funds and do not maintain a fund balance because expenditures are always equal to and offset revenues. For example, this includes vendor activity such as revenues and expenditures for Aramark's services.

This category corresponds to Fund Type 81 within Chart 1 of WWU's Chart of Accounts.

These funds do not maintain a fund balance.

This category is fund type 'BF" within Western's Chart of accounts.

Liability funds exist within Western’s State Operating and Auxiliary fund types but are categorized separately in this discussion because they are unique. By law, Western is required to show total liabilities on the financial statements. Conceptually, this amount represents Western’s total liability for leave accrual, retirement plans, and healthcare plans. The amount shown is an estimate of total liability as determined through actuarial procedures.

This category contains activity for specific funds within Fund Types 11 and 31 for Chart 1 in WWU's chart of accounts.

Table 4.3 Fund Balance by Fund Type

Fund balance for all fund types, including investment funds and funds used for accounting purposes.

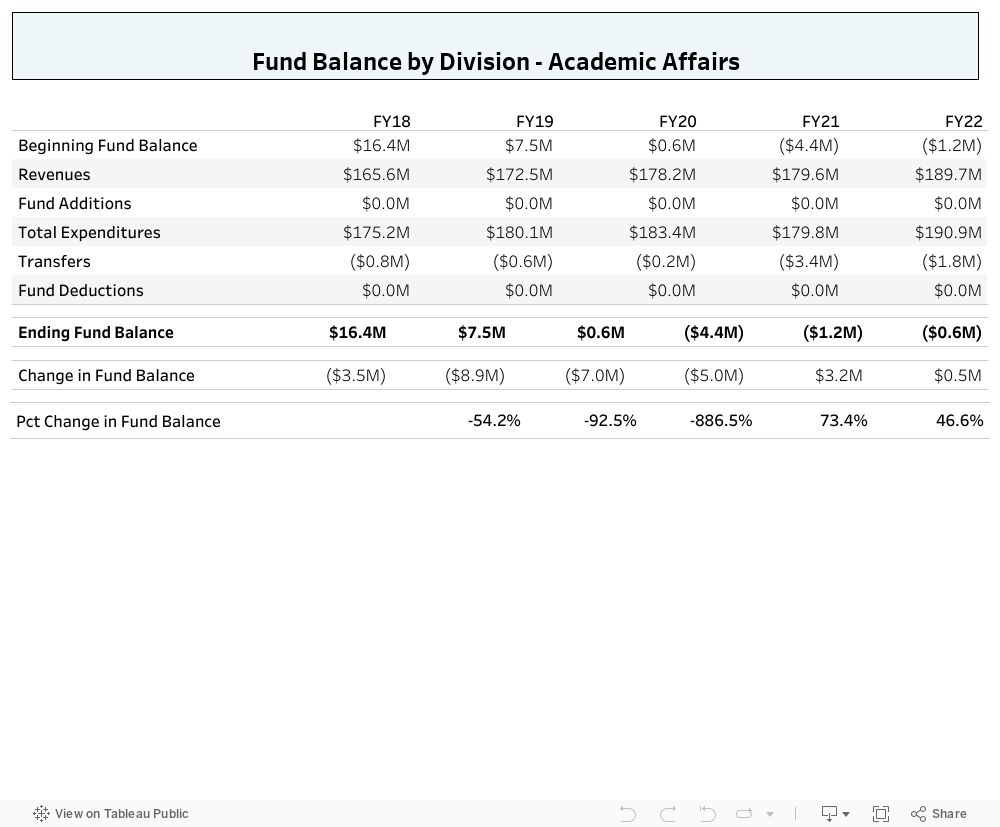

4.4 Year End Fund Balance by Division

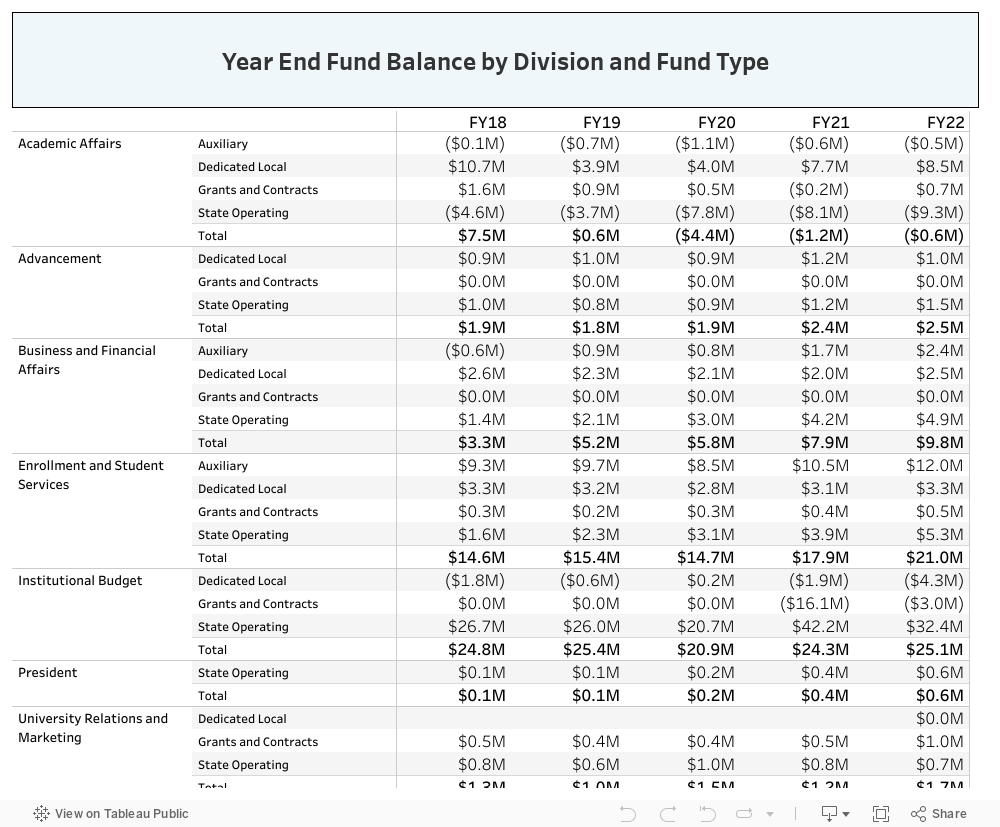

This table presents year end fund balances by division with a focus on funds that support divisional operating budgets: State Operating Funds, Dedicated Local Funds, Auxiliary Funds, and Grants and Contracts. As such, the figures presented below will not match the ending fund balance totals as presented on the Financial Statements with the exclusion of non operating fund types.

Table 4.4 Year end fund balance by Division and Fund Type

Divisional Fund Balance Tables

Select a division below to view the corresponding fund balance table. Fund balance tables Fund balance reflect state operating, dedicated local, auxiliary, and grants and contracts fund types.

4.5 Institutional Fund Balance: Pressures and Constraints

Beginning in FY 2020, the University operating budget assumed a recurring deficit of $2.4 million. A planned use of one-time funds to cover the shortfall between revenues and expenses on an annual basis was assumed until tuition revenues from enrollments (primarily growth in non-resident students) could grow to address the recurring gap. However, enrollment losses from the COVID-19 pandemic starting in Spring quarter of 2020 significantly increased the recurring operating deficit, with temporary federal stimulus funds bridging the gap. With reduction in enrollments, the University has lost its ability to maintain a buffer between planned and budgeted tuition revenues which previously contributed to institutional reserves.

With stimulus funds planned to be fully utilized by FY 2023, the University is implementing permanent reductions to its operating budget, with plans to fully close the recurring budget deficit by FY 2025. This phased-in approach, plus a flat enrollment outlook into the foreseeable future, puts pressure on the University’s ability to maintain its current level of Institutional reserves, as use of fund balance may be needed to help gradually implement reductions without layoffs or impacts to student access.

The Finance, Audit and Risk Management Committee of the University’s Board of Trustees provides general guidance around maintaining adequate reserves to support financial health and ability to sustain operations through enrollment fluctuations or unforeseen factors affecting revenues. This guidance supports an uncommitted reserve target of 10% of the state/tuition funded operating budget.