Chapter 3: FY 2020-21 Expenditures

3.0 Expenditures: Chapter Overview

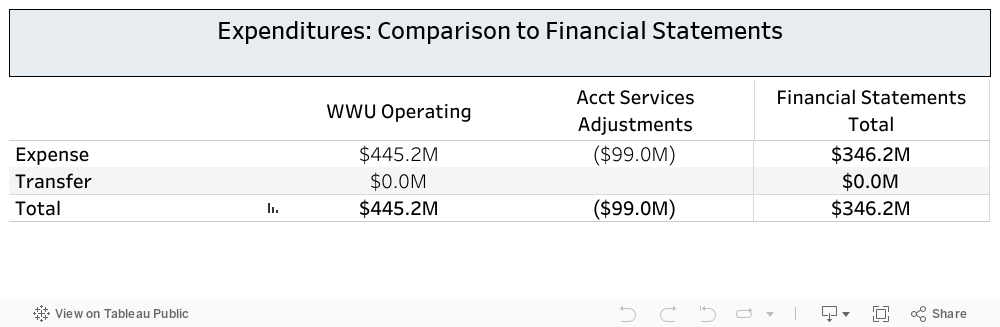

3.1 WWU Expenditures Compared to Financial Statements

- State Operating Funds

- Dedicated Local Funds

- Auxiliary Funds

- Internal Service Funds

- Grants and Contracts Funds

- Loan Funds

- Agency Funds

- Capital Facilities

3.3 Expenditures by Functional Classifications

3.4 Expenditures by Natural Classifications

3.5 Expenditures by Division and Department

3.6 Capital Facilities Expenditures

3.1 WWU Expenditures Compared to Financial Statements

Similar to revenues, expenditures reported on the Financial Statements include WWU Operating expenditures and year-end adjustments made by Accounting Services to fulfill mandatory reporting requirements. The purpose of presenting these figures is to show how expenditure totals in the Financial Statements are derived and demonstrate how expenditure totals in this document both relate to and differ from the financial statements. The remainder of this subsection reports WWU Operating (Chart 1) expenditures and transfers only.

Table 3.1 Comparison to Financial Statements

Examples of adjustments made by Accounting Services include:

- Elimination of double-counted expenditures across departments: For Financial Statements reporting, expenditures are required to be counted only once. However, in this document (as with any management reports) expenditures are reflected for each unit that the expense occurred. For example, if a department incurs an expense for facility maintenance, this expense would show in Western’s chart of accounts both in the department needing the maintenance and the expense shows within Facilities Maintenance for incurring the expense for performing the work. On the financial statements, this type of scenario would show expenditures only occurring once whereas we present those expenditures in both departments because this reflects the impact to each department’s budget.

- Depreciation of capital assets. Depreciation of capital assets are recorded in Western’s chart of accounts according to a depreciation schedule entered by Accounting Services. For Financial Statements reporting, this is eliminated as an expense.

- Reclassifying staff waivers as benefits expense. Staff participating in the state tuition waiver program receive tuition waivers for attending courses. This is reported as a reduction to tuition revenue in this document but for financial reporting purposes, the financial statements reclassify this reduction in revenue as a labor expense because it is an employee benefit.

Please note that transfers are discussed in a separate subsection below . Transfers do not change total expenditure amounts but do have the net effect of reducing or increasing expenditure totals across categories (e.g., across departments).

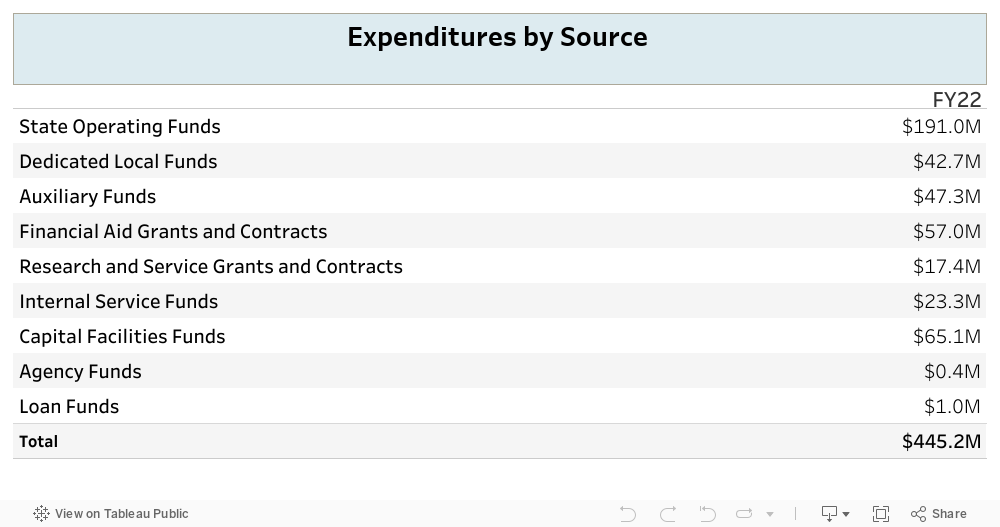

3.2 Expenditures by Fund Type (Source)

The remainder of this chapter focuses on WWU Operating expenditures only (Chart 1) and does not include the adjustments made by Accounting Services for WWU's annual financial statements. In FY 2021, total expenditures were $461.7 million when considering all funds. Each fund source is purposed for certain expenditures and has restrictions on use. We describe these fund types in more detail below, including what kinds of expenditures fall within each category.

Table 3.2 Expenditures by Fund Type (Source)

Click on a category below to read more detail.

State Operating Funds represents both state appropriated dollars and tuition operating dollars and is to be used for expenses related to the university’s primary mission such as salaries, goods and services, travel, and equipment.

State Operating funds are defined in WWU's Chart of Accounts as all expenditures in Chart 1 for fund types 11 and 14.

Dedicated Local funds are established to fulfill specific objectives where approved fees can be charged to cover the costs of the program. Fee revenue in a self-sustaining fund is only be used for the purpose the fund was established.

Dedicated Local funds are defined in WWU's Chart of Accounts as all expenditures in Chart 1 for fund type 12.

Auxiliary funds are for business-type entities (Campus Recreation, Housing and Dining, Parking, Bookstore) which serve the university community and whose main source of revenue is not tied to the university’s primary mission. Expenditures in this category are directly related to the needs of the Auxiliary units.

Dedicated Local funds are defined in WWU's Chart of Accounts as all expenditures in Chart 1 for fund type 31.

Internal Service funds are established to charge departments of the university their portion of shared expenses such as telephone, data services, utilities, and computing expenses.

Internal Service funds are defined in WWU's Chart of Accounts as all expenditures in Chart 1 for fund type 13.

Grants and Contracts funds are established to track the activity relating to each grant and contract. These include research grants from Federal, State, and Local governments (Fund Type 21), financial aid money (Fund Type 22), and Service grants and contracts (Fund Type 23) where an outside entity has some oversight or expectation of how the funds are spent. Grants & Contracts are reported in two categories: Financial Aid Grants & Contracts and Other Grants & Contracts (Research and Service).

Financial Aid Grants and Contracts funds are defined in WWU's Chart of Accounts as all expenditures in Chart 1 for fund type 22.

Research Grants and Contracts funds are defined in WWU's Chart of Accounts as all expenditures in Chart 1 for fund type 21, and Service Grants and Contracts correspond to those expenditures in Fund Type 23.

Loan funds include expenditures for WWU student financial aid loans and expenses related to administrative and asset management fees of quasi-endowments and endowments.

Loan funds are defined in WWU's Chart of Accounts as all expenditures in Chart 1 for fund types 41, 51, 61.

This category is a broad inclusion of expenditures for funds tied to Capital Facilities and includes major capital projects, building fee funded projects, preventative maintenance, and institutionally funded projects. We also include debt service and depreciation in this category.

We discuss capital facilities expenditures in greater detail in Section 3.6.

Capital Facilities Expenditures as discussed in this document reflect expenditures in Chart 1 for the following fund types: 91, 92, 93, 94, 95, 96, 97

Agency funds are pass-through funds. As such, the revenues and expenditure amounts in any given year are equal and offset, and largely are comprised of payments to WWU vendors such as Aramark.

Agency funds are defined in WWU's Chart of Accounts as all expenditures in Chart 1 for fund type 81.

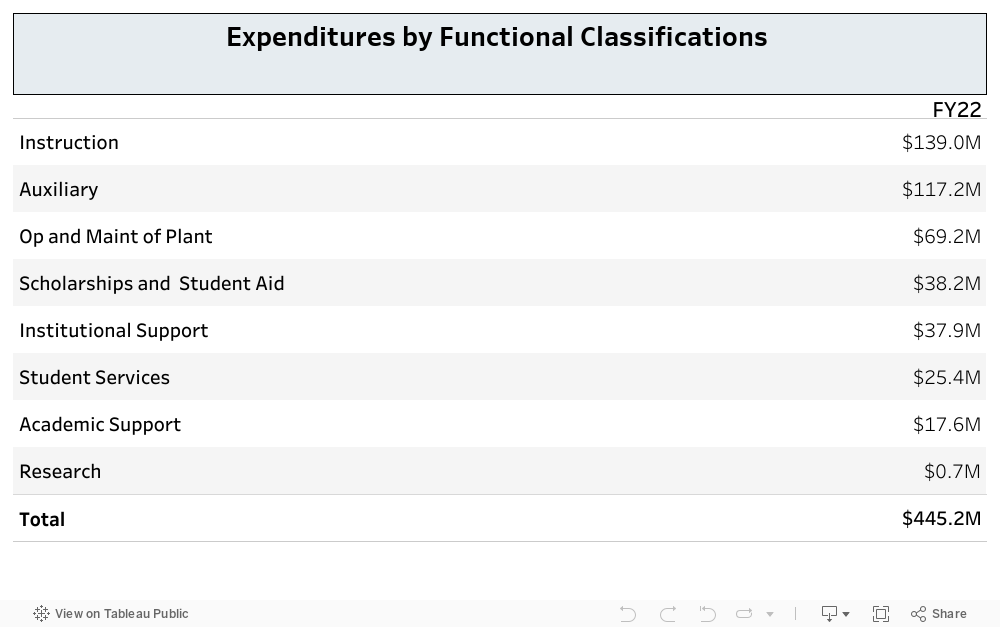

3.3 Expenditures by Functional Classifications

The functional expense classification is a method of grouping expenses according to why an expense was incurred rather than what was purchased. Classifications are defined according to the Financial Accounting and Reporting Manual (FARM) for Higher Education and include the following categories:

- Instruction: This category largely includes salaries and benefits for faculty and staff for academic instruction.

- Research: This category includes labor expenses for faculty for research projects, and specialized equipment purchases for research.

- Academic Support: This category includes expenses for IT support, Western Libraries.

- Student Services: This category includes expenses for student service areas such as the Tutoring Center and Advising and Career Services)

- Institutional Support: This includes expenditures for departments that support Western’s Internal operations such as Institutional Research, the Equal Opportunity Office, Internal Auditor, Accounting Services, and the Student Business Office.

- Operation & Maintenance of Plant: Includes expenses for services performed by Facilities Maintenance, other maintenance costs and capital projects.

- Scholarships and Student Aid: Includes expenses for WWU aid awarded to students such as Departmental Grants. Pass through funds awarded to students are also included here, such as Washington College Grant.

- Auxiliary: This captures expenses related to self-sustaining auxiliary enterprises, such as Housing and Dining, and the Bookstore.

Functional Classification categories are derived from the Program Codes used in Western’s Chart of Accounts. For more detailed information on functional expenses, please visit the NACUBO website.

Table 3.3 Expenditures by Functional Classifications

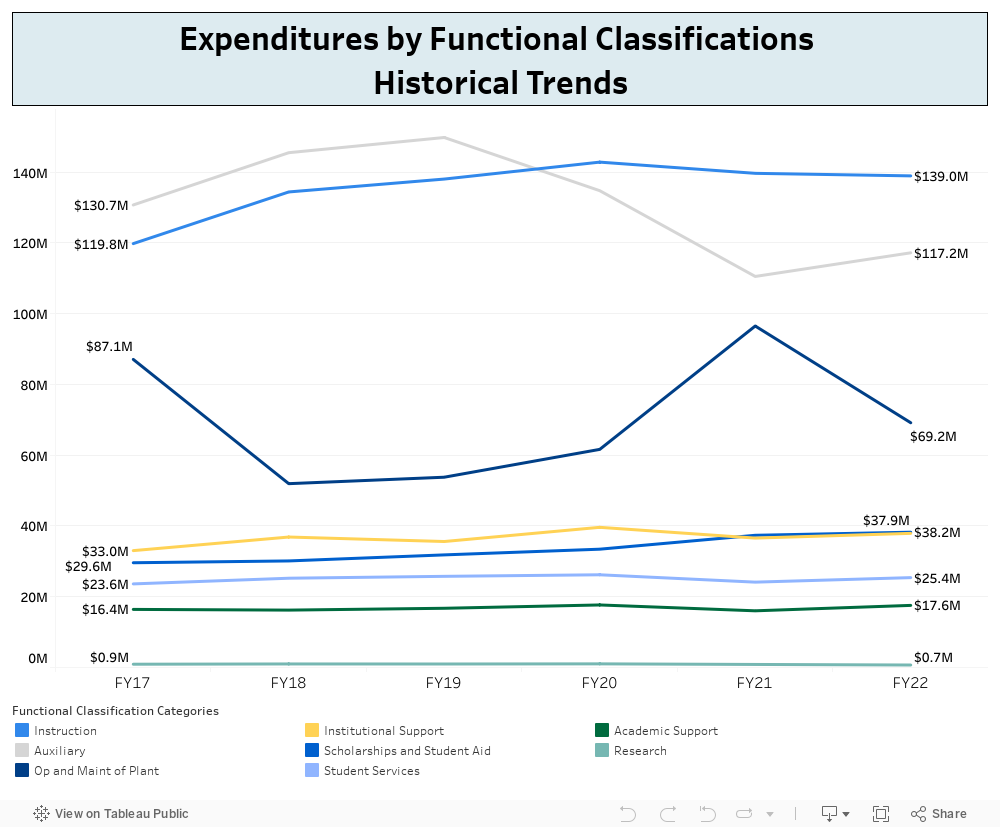

Western has generally seen an increase in costs related to Instruction, primarily salary and benefit costs both from increased FTE for faculty and staff, as well as wage increases over time (Figure 3.3). However, the COVID-19 pandemic resulted in changes to these trends. WWU implemented a 3 percent one-time reduction to recurring divisional budgets during FY 2021, as well as hiring restrictions during that time. Enrollment decreases and a remote learning environment led to decreased auxiliary expenditures for both FY 2020 and 2021.

Figure 3.3 Historical Trends in Expenditures by Functional Classifications

Expenditures by functional type for the past five fiscal years.

Expenses related to Capital Projects ("Op and Maint of Plant) tend to vary widely over time, depending on the number of capital projects under construction during a given year. In FY2021, the construction of the Interdisciplinary Sciences building and the Alma Clark Glass Hall projects were under way with expenditures reflecting payments for the contracting work. Please note that Research expenditures appear lower in this view compared to the Financial Statements - this is because we only report Chart 1 expenditures here whereas the Financial Statements reclassify some Grants and Contracts expenditures related to Instruction as Research if the purpose of the grant is related to research.

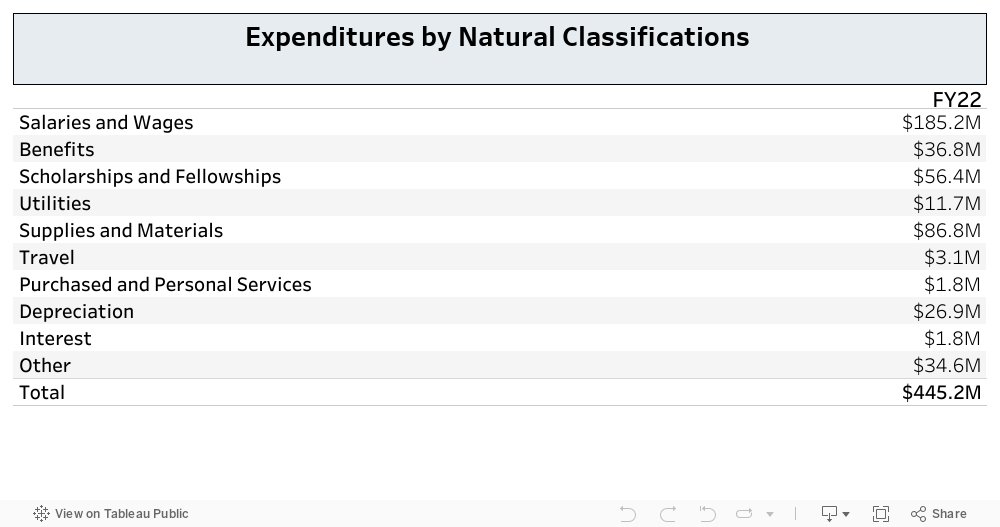

3.4 Expenditures by Natural Classification Categories

Natural Classification Expense categories group expenses according to the type of costs incurred. The purpose is to show what was purchased rather than why the expense occurred. Classifications are defined according to the Financial Accounting and Reporting Manual for Higher Education and include the following categories:

- Salaries & Wages: This includes all expenses paid to faculty, staff and student employees regardless of full time status.

- Benefits: This includes all benefits such as retirement or healthcare costs paid to faculty, staff, and student employees.

- Scholarships & Fellowships: This includes scholarships and aid awarded to students.

- Utilities: This captures expenses such as heating, electricity and internet needs.

- Supplies & Materials: This category includes all goods and services purchases.

- Travel: This includes all travel-related activities.

- Purchased and Personal Services: This category includes expenses for contracted services for legal, custodial, repairs, printing or other services.

- Depreciation: This category captures depreciation of property, equipment, and assets.

- Other: This category includes miscellaneous other expenses such as capitalized fixed assets, debt service, and personalized expense.

Natural Classification categories are derived from the Account Type Codes used in Western’s Chart of Accounts. For more detailed information on Natural Classification of expenses, please visit the NACUBO website.

Table 3.4 Expenditures by Natural Classification

Expenditures by purpose as defined by the natural classification categories.

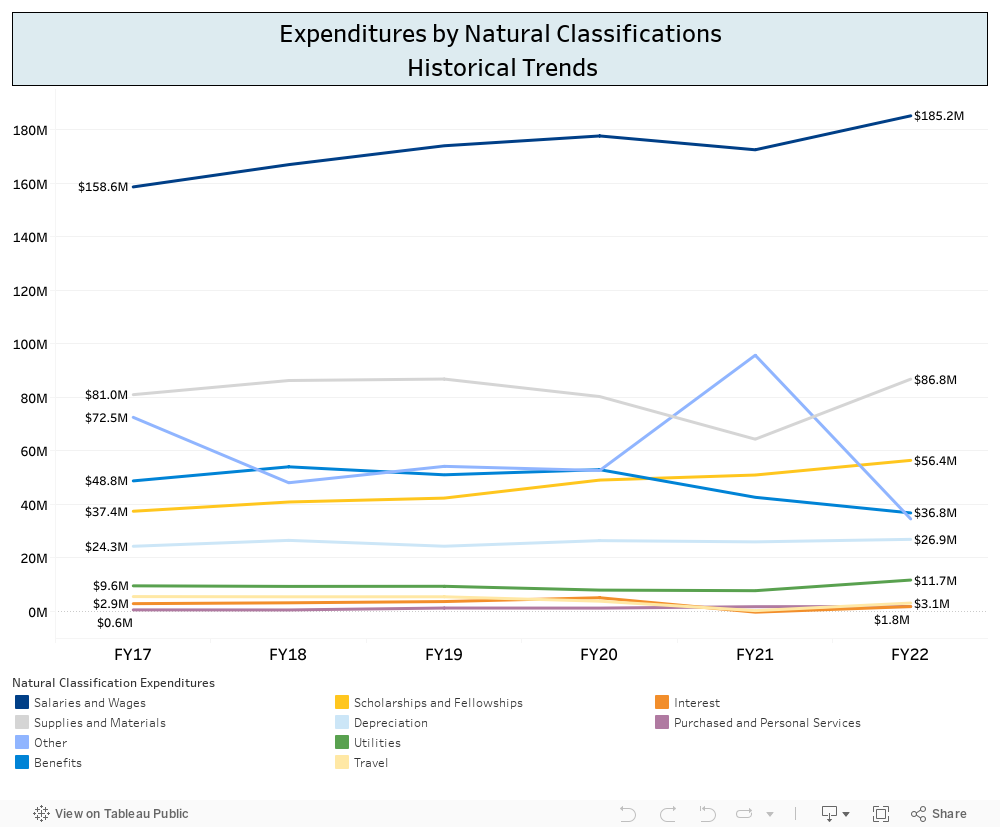

Generally, expenses in these categories have been fairly consistent over time except for changes in FY 2020 and 2021 related to the COVID-19 pandemic. During the pandemic years, expenses for supplies and materials as well as travel dropped considerably as departments worked to reduce expenses by limiting these purchases and mandated travel restrictions nearly eliminated all travel opportunities. Additionally, Western implemented hiring restrictions that increased vacancies and reduced salary and wage expenses. Stimulus funding for student financial aid and increased funds in some state funded programs such as the Washington College Grant has resulted in increased awards for students, with $51 million in Scholarships and Fellowships awarded during FY 2021. Expenses in the "Other" category increased substantially in FY 2021 due mainly to the increase in capital projects expenditures related to the construction of the Alma Clark Glass Residence Hall and the Interdisciplinary Sciences building.

Figure 3.4 Expenditures by Natural Classifications Historical Trends

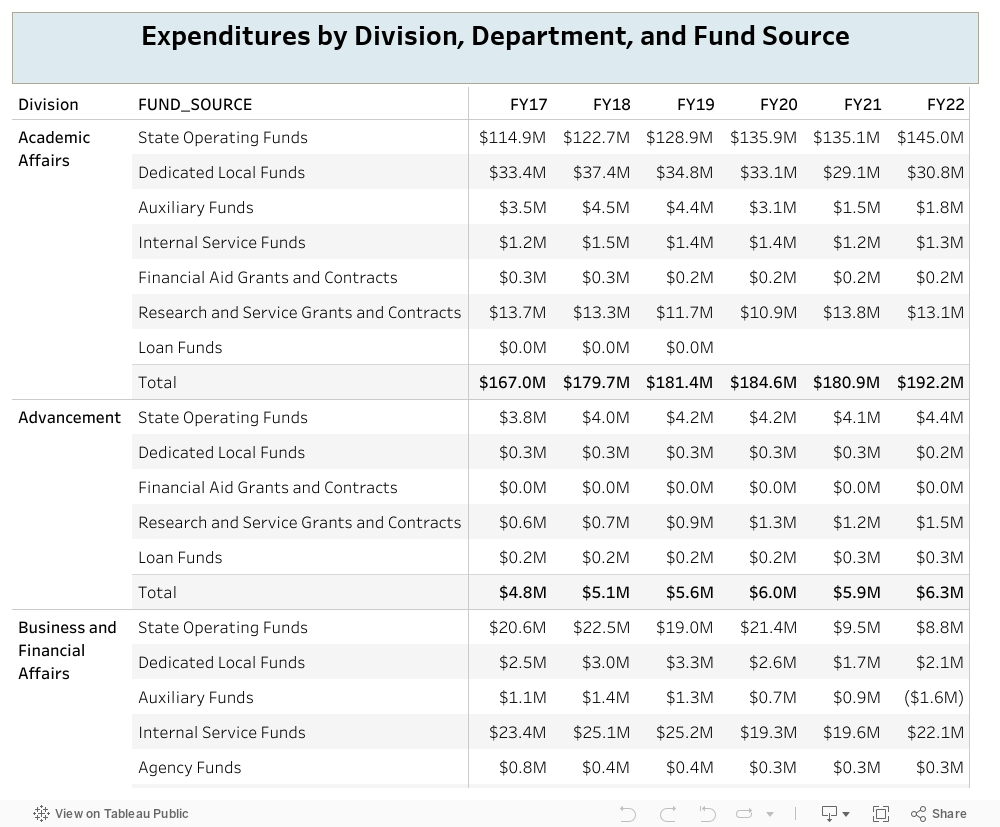

3.5 Division and Department Expenditures by Fund Type

As described in Chapter 2, Western's divisions receive revenues from multiple funding sources which reflects the operations of each division. Expenditures on state operating funds (state appropriations and tuition dollars) reflects the direct investment of state funds that support Western’s core mission. Additional services are reflected through self-sustaining funds or managed funds that are passed on to students such as student financial aid grants.

Table 3.5 Division and Department Expenditures by Fund Source

Divisional expenditures by funding sources.

This is an interactive table; to see department level expenditures, hover your cursor over "Division" until a "+" symbol appears.

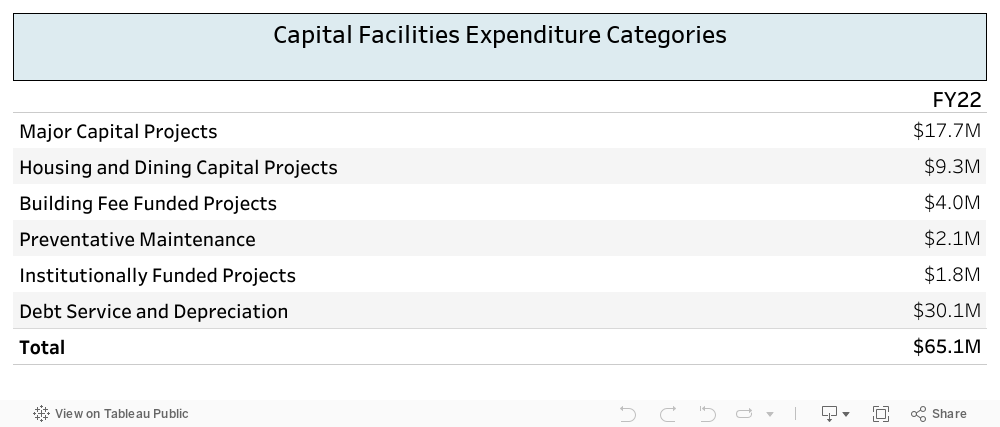

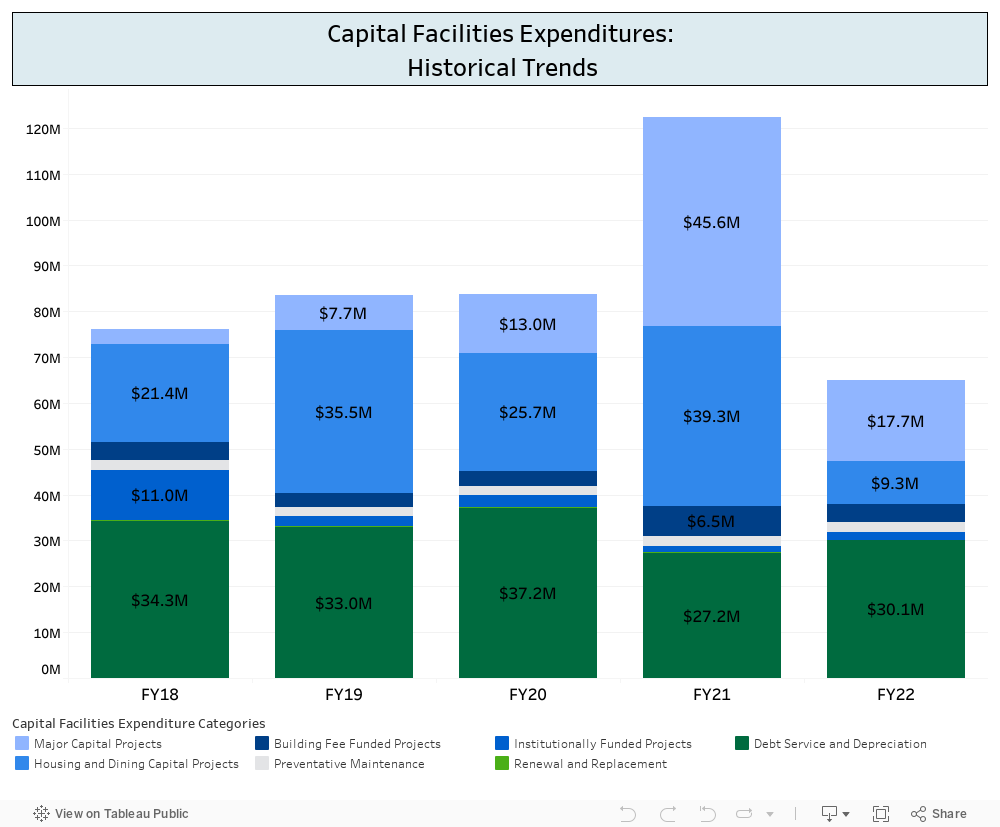

3.6 Capital Facilities Expenditures

Capital Facilities Expenditures as categorized in this document reflect expenditures for major and minor capital projects, housing and dining capital projects, preventative maintenance, and depreciation of capital assets. These categories are discussed in more detail below. For additional information, please see the Capital Planning and Development website.

Table 3.6 Capital Facilities Expenditures

Capital Facilities Categories

Select a category below to learn more about that nature of the expenses and associated FY 2021 activities.

Major capital project expenditures are state-support project expenditures for state funded capital projects and the majority of FY 2021 expenditures (approximately $41 million) were for the construction of the new Interdisciplinary Sciences Building.

The "Major Capital Projects" expenditure category is defined as all expenses in Fund Type 93 under Chart 1 in WWU's Chart of Accounts.

In FY 2021, the Housing and Dining Capital Project expenditures were for the construction of the new residence hall, the Alma Clark Glass Hall. The remaining expenditures were for various enhancements and upgrades to existing residence hall facilities.

The "Housing and Dining Capital Projects" expenditure category is defined as all expenses in Fund Type 92 under Chart 1 in WWU's Chart of Accounts.

Building Fee Funded projects are for campus-wide minor works preservation and programmatic improvements, campus-wide classroom and lab upgrades, and some preventative maintenance. As an example, in FY21 this included expenditures for ADA upgrades to WWU elevators.

The "Building Fee Funded Projects" expenditure category is defined as all expenses in Fund Type 94 (excluding Funds 94501/94502 which are considered under "Preventative Maintenance") under Chart 1 in WWU's Chart of Accounts.

The Preventative Maintenance category primarily pays for labor costs for various units within Facilities Management (e.g., Academic Maintenance Shop, Outdoor Maintenance, Plumbing and Electrical Shops). These funds are state-appropriated and purposed for the ongoing maintenance of existing WWU facilities.

The "Preventative Maintenance" expenditure category is defined as all expenses in under funds 94501 and 94502 under Chart 1 in WWU's Chart of Accounts.

Institutionally Funded Projects include additional support purposed for specific projects and funded by Institutional or Foundation funds. In FY 2021, this included approximately $700,000 for the pre-design of the new Electrical Engineering and Computer Sciences building and $500,000 for renovations to Old Main.

The "Institutionally Funded Projects" expenditure category is defined as all expenses in Fund Type 91 under Chart 1 in WWU's Chart of Accounts.

The bulk of Renewal and Replacement (R&R) expenditures are actually recognized as transfers and are discussed in more detail in the next section. In FY 2021, there was approximately $300,000 in R&R activity for the Campus Recreation Center.

The "Renewal and Replacement" expenditure category is defined as all expenses in Fund Type 96 under Chart 1 in WWU's Chart of Accounts.

Debt Service and Depreciation expenses are recorded by Accounting Services for financial reporting purposes. Generally, these expenses reflect depreciation of various facilities assets. Also included is debt service for the certification of participation sale associated with the Carver Facilities renovation.

The "Debt Service and Depreciation" expenditure category is defined as all expenses in Fund Types 95 and 97 under Chart 1 in WWU's Chart of Accounts.

Capital expenditures were higher than normal in FY 2021 primarily because there were two major capital projects under construction, the Interdisciplinary Science Building and the Alma Glass Residence Hall. Expenditures are expected to be substantially reduced in FY 2022 due to the closing of these major projects.

Figure 3.6 Capital Facilities Expenditures Historical Trends

3.6.2 Operating Reserves Purposed for Capital Projects

On occasion, Western uses operating reserves to complete essential capital projects that did not receive full state funding or are not covered through the state funding model. In FY 2021, this totaled $571,819 across three projects.

The most significant project funded this way in FY 2021 was addressing preservation and programmatic needs in Old Main 120 ($561,502). On the programmatic side, this project provided modern administrative space for the Student Business Office, Policy and Public Records, Internal Audit, and the Assistant Attorney General’s office. The space is flexible enough to allow collaboration and privacy as needed for these administrative functions. On the preservation side, this project repaired water damage and provided water mitigation to an area of the building that was previously subject to water infiltration. The project also provided improvements to ventilation and electrical systems.

The remaining $10,317 in FY 2021 capital project support was incurred for office space and the Honors space conversion in Old Main.

3.7 Transfers

Transfers do not change the overall total expenditure amounts but have the net effect of increasing or reducing expenditure totals across categories. For example, a transfer of expenditure activity from one department to another will sum to zero across departments, but one department will show an increase in expenses whereas the other will show a reduction.

Transfers are included in this chapter but discussed separately in this section because this activity is important to acknowledge in the overall picture of expenditures.

3.7.a Types of Transfers

Transfers are use for one-time support and moving expenses between funds. Common types of transfers include:

- One time funding to divisions from the institutional budget

- Institutionally funded capital transfers

- Stimulus funding

- Transfer of expenses between self-sustaining and state-funding fund types

- Renewal and replacement of assets and bond payments

3.7.b Major FY21 Transfers

In FY 2021, the most significant transfers involved stimulus funding support that was applied to offset revenue losses from the pandemic. Those transfers had a net impact of $9.1 million to state operating funds. Additionally, $1.5 million was transferred into the institutional state operating funds as a treasury loan to pay for essential IT network infrastructure, with an associated payback plan over several years.

An additional $333,541 total was transferred out of state operating for a variety of smaller needs, such as:

- Distribution of the institution’s share of cash balance from the Federal Perkins Loan Fund that was returned to the University and transferred to Institutional Reserves;

- Bond repayment support from the Institutional Budget to Housing and Dining for construction of the Multicultural Center;

- Transfer of funds from Institutional Budget to Retirement of Indebtedness fund for Lincoln Creek debt service payments;

- Payment to Whatcom Transportation Authority for reduced bus fare subsidy.